AITA for canceling my life insurance policy because my husband won’t make a beneficiary on his?

Welcome back, AITA devotees! Today's story plunges us into the complex world of marital finances and the often-overlooked necessity of life insurance. It's a topic that can spark heated debates, touching upon trust, responsibility, and the long-term security of a family. When one partner feels their future isn't being adequately protected, what lengths are they justified in going to make their concerns heard?

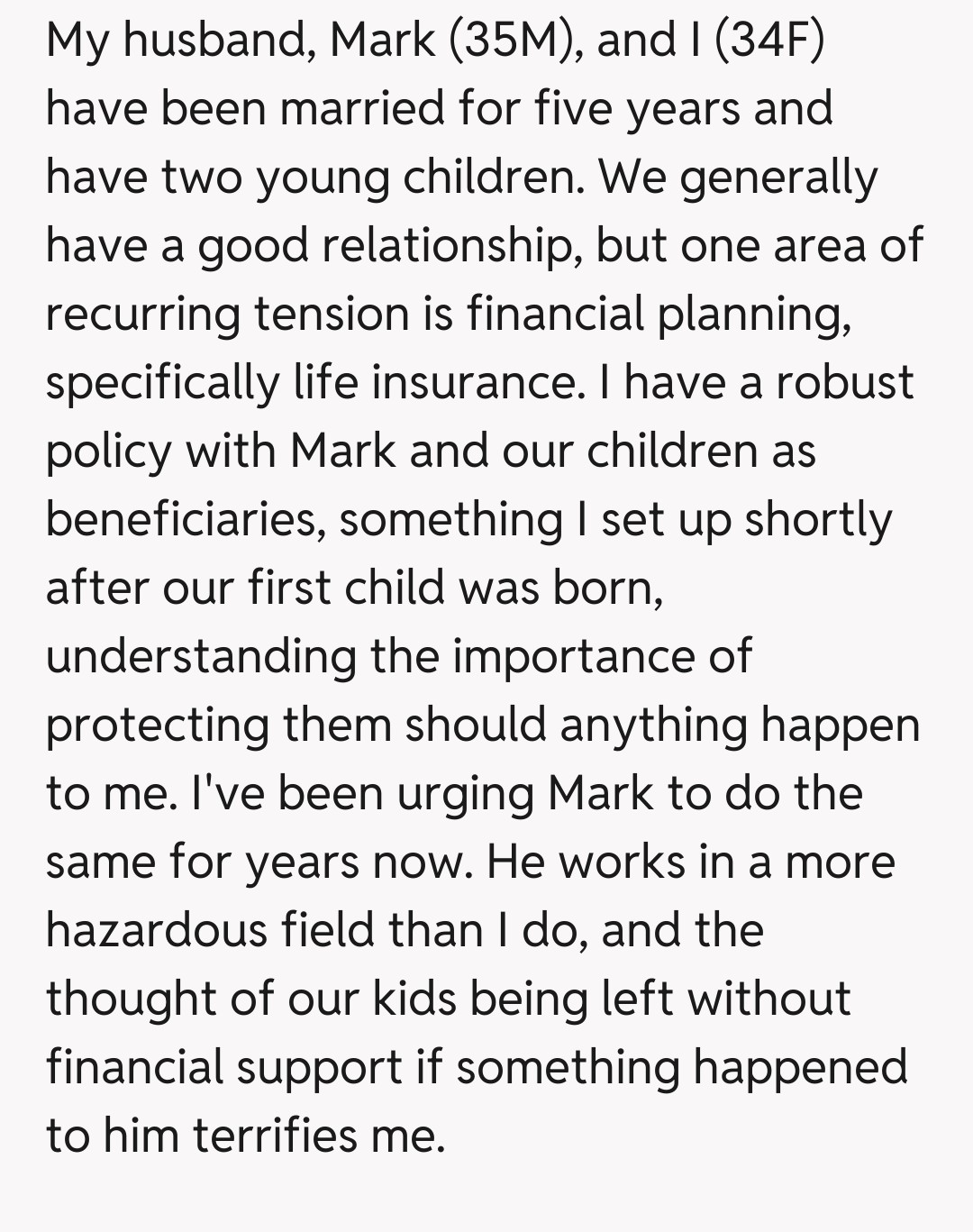

Our original poster, a woman feeling increasingly anxious about her family's financial future, brings a scenario to the table that many couples might silently grapple with. The core of her dilemma revolves around a crucial financial safety net – life insurance – and a disagreement with her husband that escalates to a dramatic and potentially irreversible decision. Let's dive into the story that asks: is reciprocal protection a basic expectation, or did she cross a line?

"AITA for canceling my life insurance policy because my husband won't make a beneficiary on his?"

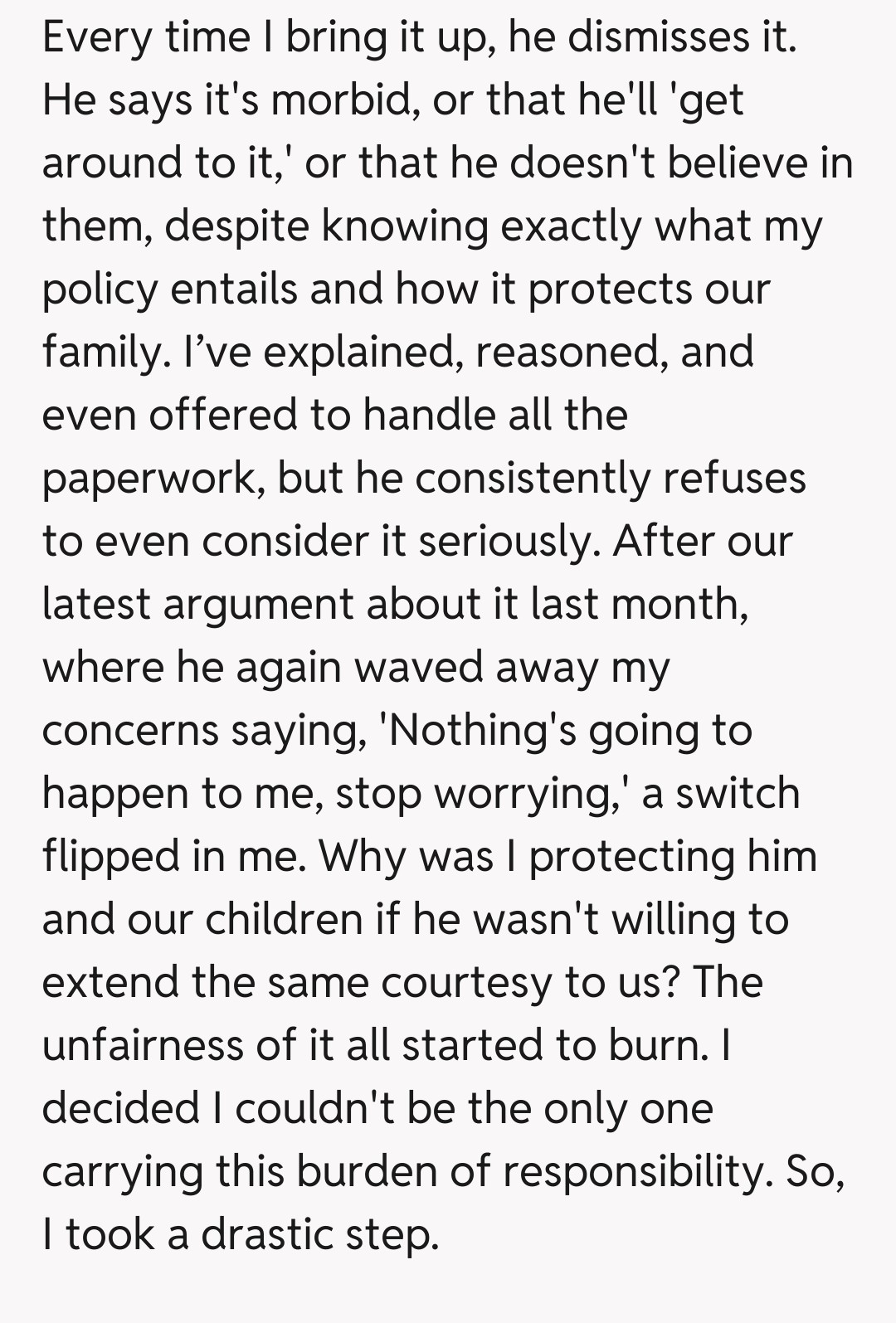

The original poster's frustration is palpable and, dare we say, understandable. Life insurance, while a grim topic, is a fundamental aspect of responsible financial planning for a family, especially when there are young children involved. The desire for both partners to contribute equally to this security net is not only reasonable but often expected. Her feeling of carrying an unequal burden for the family's future, particularly when her husband works in a more hazardous field, holds significant weight.

However, the husband's perspective, though perhaps poorly articulated, also needs consideration. His dismissal of the topic might stem from various places: a genuine discomfort with mortality, a lack of understanding about insurance mechanics, or even a deeper issue of trust or control within the relationship. While none of these fully excuse his inaction, they highlight that the problem might be more complex than simple negligence, requiring a different approach.

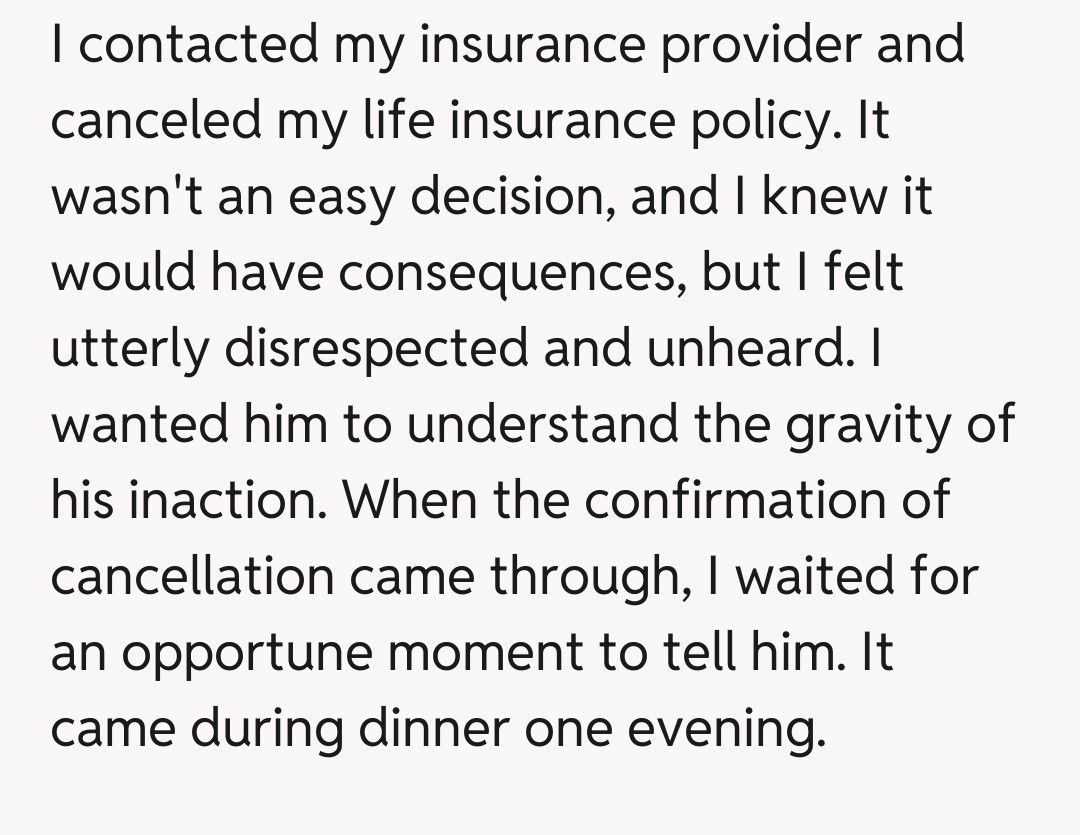

The core of the conflict shifts when the OP decides to cancel her own policy. On one hand, it's a desperate move to get her husband to understand the gravity of her concerns and the reciprocal nature of partnership. She's essentially saying, "If you won't protect us, I won't protect you." This tit-for-tat can feel justified when one partner feels ignored or taken for granted in crucial areas.

On the other hand, canceling a policy that benefits her children as well, effectively removing a layer of security for them, opens the door to arguments of being equally irresponsible or even punitive. While her motivations might have been to shock her husband into action, the immediate outcome is a reduction in the family's overall financial safety net. This makes the situation exceptionally complex and leaves many debating whether her actions were justifiable.

Is this strategic or just spiteful? Unpacking the life insurance drama.

The comments section on this one was absolutely on fire, with a fairly even split between those who felt the OP was justified and those who thought she escalated things too far. Many 'NTA' votes centered on the principle of fairness and shared responsibility. Readers argued that the husband's refusal to protect his family was a massive red flag and that the OP was simply mirroring his lack of commitment to their shared future, thus forcing him to confront the consequences of his inaction directly. His 'morbid' excuse really didn't fly with the commenters.

Conversely, the 'YTA' and 'ESH' contingent pointed out that two wrongs don't make a right. They emphasized that the cancellation ultimately harms the children by removing a layer of financial protection, regardless of the husband's stubbornness. These commenters suggested alternative approaches, like seeking couples counseling or financial mediation, rather than taking a punitive action that leaves the entire family more vulnerable. The debate highlighted the fine line between standing your ground and creating more problems.

This intense AITA story serves as a stark reminder that financial decisions are rarely just about money; they're often deeply intertwined with trust, respect, and shared values within a relationship. While the OP's frustration is clear, and many sympathize with her feeling unheard, the chosen resolution created new vulnerabilities for her family. Ultimately, this situation underscores the critical need for open, honest communication and a unified approach to family planning. Perhaps an impartial third party, like a financial advisor or marriage counselor, could help bridge this significant gap in understanding and rebuild trust. It's a tough spot, and we hope they find a way forward.